KRA Introduces Automated Export VAT Reporting Through iCMS and iTax Integration

How KRA’s iCMS–iTax integration will automate export VAT reporting and what businesses must do to stay compliant ahead of rollout this month.

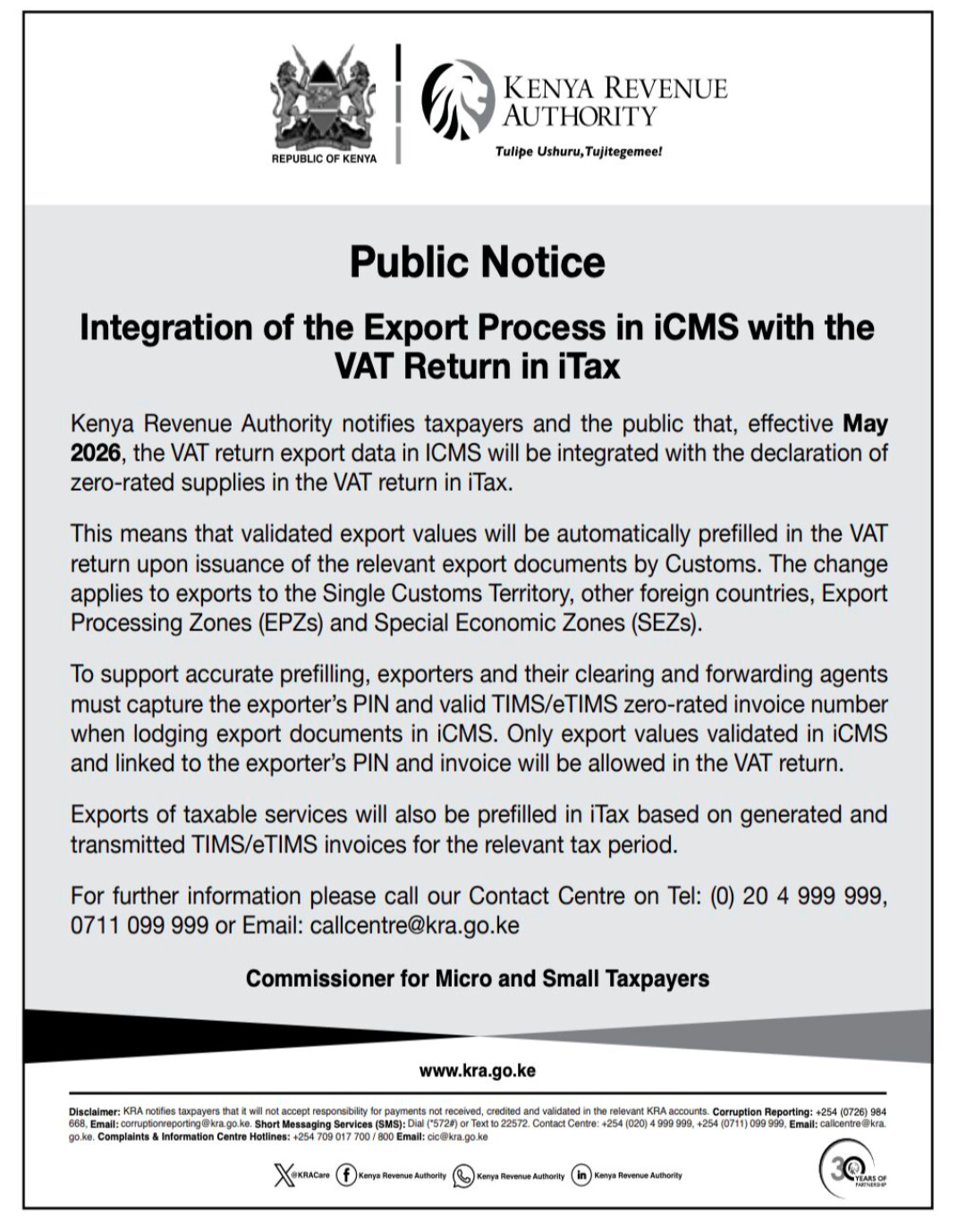

The Kenya Revenue Authority (KRA) has announced a major shift in how export sales will be reported for Value Added Tax (VAT) purposes in Kenya. In a public notice issued on 23rd April 2026, the tax authority outlined plans to automate and tighten controls around export reporting by integrating two critical systems already used by exporters: iCMS(Integrated Customs Management System) and iTax.

The change, which takes effect this month, marks another significant step in KRA’s broader push toward digital tax compliance and automation.

What Is Changing?

Previously, exporters were required to manually capture export sales figures when filing VAT returns on iTax, even after processing export declarations through iCMS (Integrated Customs Management System).

Under the new system integration:

Export data processed through iCMS will automatically flow into iTax.

Export sales values will be auto-populated in VAT returns.

Exporters will no longer manually input export figures under zero-rated supplies.

VAT reporting will now rely directly on validated customs records.

Since exports are classified as zero-rated supplies for VAT purposes, the values will automatically appear in the relevant section of the VAT return once Customs validates the export documentation.

Why This Integration Matters

The integration is designed to improve:

1. Accuracy in VAT Reporting

By pulling data directly from customs records, KRA aims to reduce discrepancies between customs declarations and VAT returns.

2. Transparency and Compliance

The automation strengthens KRA’s ability to verify that declared exports are legitimate, properly documented, and correctly linked to the taxpayer filing the VAT return.

3. Reduced Manual Errors

Manual data entry often creates inconsistencies, omissions, or mismatches. Automated reporting minimizes these risks while simplifying the filing process for compliant exporters.

Key Compliance Requirement for Exporters

While the automation simplifies reporting, it also introduces stricter validation controls.

For export transactions to successfully reflect in iTax:

The exporter’s PIN must be correctly captured in iCMS.

The correct eTIMS invoice number must be included during export declaration.

Customs entries must be properly validated and processed.

The integration system will use these details to match customs records with the taxpayer’s VAT profile.

If any of this information is missing, incorrect, or inconsistent:

The export transaction may fail to appear in the VAT return.

Businesses could experience reconciliation challenges.

VAT refund claims may be delayed or questioned.

Additional compliance risks could arise during audits or reviews.

The Role of Clearing and Forwarding Agents

This transition also places greater responsibility on clearing and forwarding agents involved in export processing.

Exporters should work closely with their agents to ensure:

Accurate capture of taxpayer PINs,

Correct referencing of eTIMS invoice numbers,

Timely validation of export entries in iCMS.

Even minor errors at the customs declaration stage could now directly affect VAT reporting outcomes.

What Exporters Should Do Now

Kenyan exporters, the new iCMS–iTax integration is now live, and businesses engaged in exports should begin reviewing their internal compliance processes.

Key action points include:

Reviewing export documentation workflows.

Verifying eTIMS invoice accuracy.

Training teams and agents on the new requirements.

Strengthening reconciliation procedures between customs and tax records.

Monitoring export entries to ensure proper validation in iCMS.